Why are small cap and value stocks outperforming as of late?

- When you’re shopping for toothpaste, you might check the price tag before heading to the counter to make the purchase. If you happen to find a 12oz tube of Colgate for $4 and a 12oz tube of Crest for $3, odds are you are going to go with the Crest – its human nature to pay less if your “expected return” will be the same. In the case of toothpaste, you’re getting fluoride from either option, but paying less makes the return on that investment higher. You care what things cost and price matters, it’s why price-tags are front and center for nearly everything you can purchase – clothes, cars, food, travel etc. This theory can and should be applied when making investment decisions as well, no matter what “environment” we’re in.

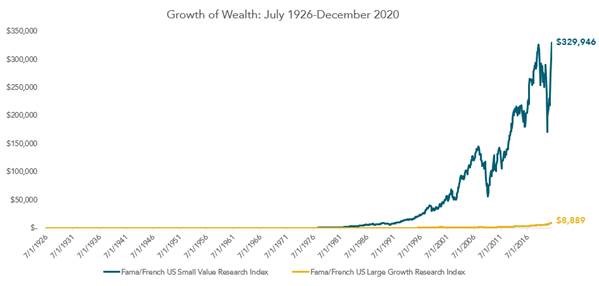

- Analysts will make the case that the recent outperformance of small cap and value stocks relative to their large cap and growth counterparts is being driven by a multitude of factors – inflation, rising interest rates, presidential policy, and economic recovery, among others. While these factors may contribute, at the end of the day it goes back to basic economic theory. We know that not all stocks have the same expected return, however, through principles of valuation and using information in prices, we can identify stocks with higher expected returns. A stock’s current price reflects information about expected future cash flows discounted by the expected return. All else equal, companies with lower relative prices (value stocks) and lower market capitalization (small cap stocks) should have higher expected returns. Exhibit 1 helps provide some empirical backing to this theory, showing the return experience of a small cap value index versus a large cap growth index. $1 invested in 1926 would have grown to $329,946 in the small cap value index, whereas that same $1 invested in the large growth index would have only grown to $8,890, a stark difference.1

- However, over the last decade, investors taking this approach to investing may have been disappointed in their returns, especially when looking across to their large cap growth brethren. The 10-year periods ending each month of 2020 were the 12 worst 10-year periods in history, when comparing small cap value stocks to large cap growth stocks. 1 It’s been a trying time for many investors, and while we expect positive small cap and value premiums every day, there are periods of underperformance, just like there are for all risk premia. Take the equity premium for example – this premium is recognized by nearly all investors, however, at the start of this century we went through a 13-year period when one-month treasury bills outperformed the S&P 500!

- For investors, rather than trying to avoid downturns or time when to get in and out of the market, you may have a better investment experience by staying disciplined so you don’t miss out on the eventual recoveries, as we have seen over recent months with small and value stocks. Exhibit 2 highlights the positive performance of a few of Dimensional’s small cap and value focused strategies. For the 6-month period ending March 2021, Dimensional’s US Small Cap Value portfolio outperformed the S&P 500 by nearly 50%! Since the end of March last Spring as a result of the COVID-19 pandemic, the S&P 500 has done well, returning 56.4%, the Dimensional US Small Cap Value Portfolio has done considerably better, returning 112.1%.2

- So, what can we expect going forward? Based on the historical data we don’t expect to experience the underperformance of value relative to growth like we did in the 2020, where the 39% differential was the greatest calendar year underperformance ever. 3 On the flip side, we also know the returns we’ve experienced in recent months may not be sustainable at the current level of outperformance. What we do know is that there is sound economic theory and robust empirical evidence that support investing in value and small cap stocks and we expect these premiums to show up every day. We also know price matters, and paying a lower price implies a higher return.

- We believe investors may be best served by making decisions based on sound economic principles supported by a preponderance of evidence. While markets and economies are constantly evolving, the theory that underpins the size and value premia is evergreen.

Exhibit 1

Past performance is no guarantee of future results. Actual returns may be lower. In USD. Indices are not available for direct investment. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment. Fama/French US Small Value Research Index: Provided by Fama/French from CRSP securities data. Includes the lower 30% in price-to-book of NYSE securities (plus NYSE Amex equivalents since July 1962 and Nasdaq equivalents since 1973) that have smaller market capitalization than the median NYSE company. Fama/French US Large Growth Research Index: Provided by Fama/French from CRSP securities data. Includes the higher 30% in price-to-book of NYSE securities (plus NYSE Amex equivalents since July 1962 and Nasdaq equivalents since 1973) that have larger market capitalization than the median NYSE company.

Exhibit 2

Performance data shown represents past performance and is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, visit us.dimensional.com.